Solutions

Solutions

Applications

Staff

Invoice Processing

Online Cash Up

Automatic Staff ID Checks

Supercharged Add ons

HR & Contracts

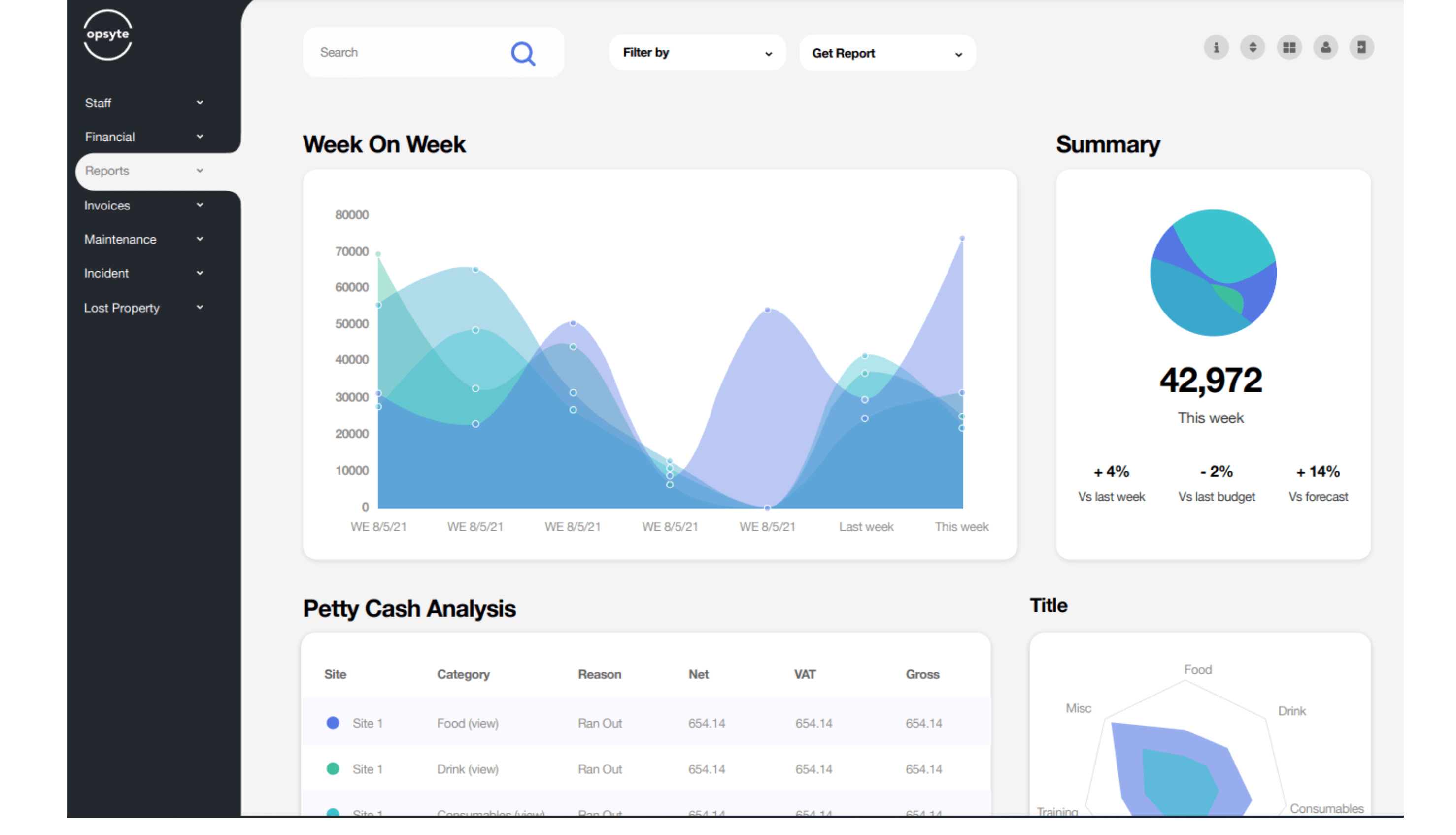

Reporting

App Advisory

Insytes

Sectors

Restaurants

Quick Service Restaurants

Pub & Bar

Company

About

Integrations

Pricing

Terms & conditions

Insytes

Applications

What are Insytes?

Reporting and Analytics

Labour Optimisation

Forecasting

Forecasting Tools

Multi Site Benchmarking

App

Resources

Help desk

Blog

Contact

Login

Book a demo

Our Blogs

Hospitality software, accounting, news, latest updates and lots more!

All

Automated Data Capture

Cash Up Online

Client Showcase

Hospitality News

Restaurant Accounting

Restaurant Reporting

Staff Rota Software

Tronc Scheme

View More

Join Opsyte and increase

your productivity.

Get Started

Join Opsyte and increase

your productivity.

Get Started

Considering Opsyte for your business? Book time with our experts now

Set up 15 minutes with our local scheduling experts to discuss how Opsyte can help you manage your team

Work Email

Phone

First Name

Last Name

Company Name

Select your country...

Type of business

Please select

Bar

Coffee Shop

Pub

Quick Service Restaurant

Restaurant

How many employees do you have?

1 - 15

16 - 49

50 - 149

150 - 749

750+

Personal information is held and processed in accordance with Opsyte's Privacy Policy. By submitting you agree to receive communications from us.

SUBMIT